Sales Tax

- Georgia Sales Tax

The Department of Revenue publishes sales tax rates for each county or jurisdiction. The state sales tax rate is 4% and each jurisdiction can add local sales taxes. Local sales taxes include, but are not limited to:Local Option Sales Tax (LOST) - 1%

Special Local Option Sales Tax (SPLOST) - 1%

Education Special Local Option Sales Tax (ESPLOST) - 1%

Transporation Special Local Option Sales Tax (TSPLOST) - 1%

Flexible Local Option Sales Tax (FLOST) - 1%

Other rates apply to Metro-Atlanta counties and jurisdictions.

Click here for the current sales tax rates.

Click here for upcoming sales tax rate changes.

Georgia voters are passing the new flexible local option sales tax in jurisdictions throughout the state.

Read more...

-

Florida Sales Tax

The Department of Revenue publishes sales tax rates for each county or jurisdiction. The state sales tax rate is 6% and each jursidiction can elect Discretionary Sales Surtax also known as county tax.

Click here for the current sales tax rates.

Forms 1099

Reporting payments to vendors.

In general, you are required to issue a Form 1099-MISC or 1099-NEC to any vendor (payee) that meets the following conditions.

- Is one of the following:

- an unincorporated business,

- an individual,

- a law firm or health care provider whether incorporated or not, or

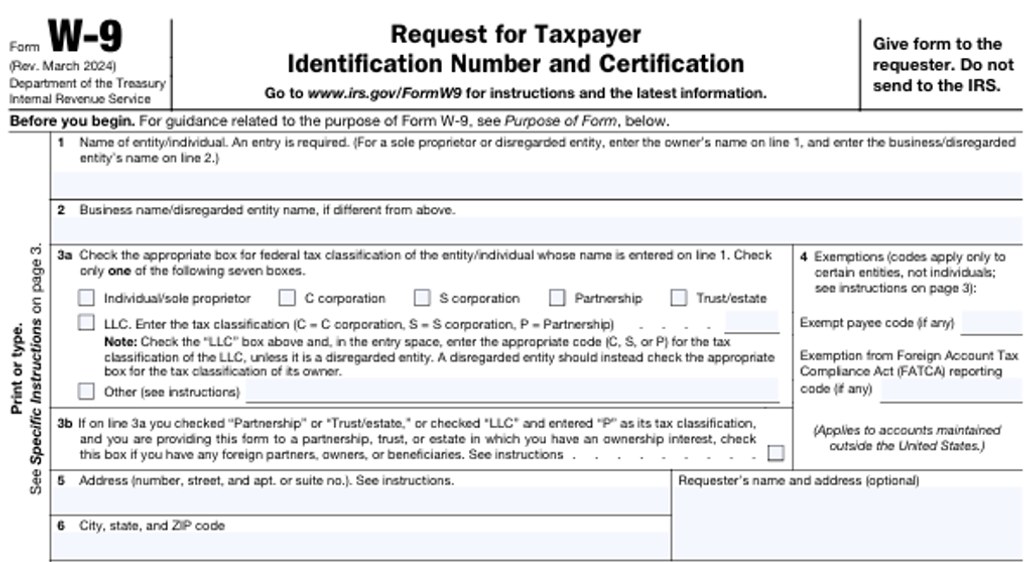

- a limited liability company (“LLC”) that is not taxed like a corporation (see Form W-9).

- That your trade or business paid a total of $600 or more in a calendar year.

- The payments were for services or rent (e.g. repair, accounting, legal, building or land rent, subcontracts, etc. including any materials provided with the service).

Obtaining Payee Information

You are required to obtain a Form W-9, Request for Taxpayer Identification Number and Certification, from each payee that meet conditions 1 and 3, above, and that may receive at least $600 in payments during the year.

If the payee refuses to provide Form W-9 then backup withholding may be required on your part. Contact our office if this is the case.

Due Dates

Generally, Forms 1099-MISC are due to your payees by January 31 of the year after payment. A $250 per form penalty can be assessed for failure to provide the forms by the due date.

Copies A of Form 1099-NEC are due to the Internal Revenue Service by January 31. An additional $250 penalty per form can be assessed for failure to file by the due date. Copies A of Form 1099-MISC are due to the IRS by February 28 if paper filing or March 31 if filing electronically.

Electronic filing is required if you file 10 or more information returns in aggregate (counting all information returns including Forms W-2 and all 1099 series forms).

Income tax returns require taxpayers to answer questions indicating their compliance with information return reporting requirements.

Worksheet Instructions

These completed worksheets must be provided to our office before January 15 in order to meet the above due dates.

Use the forms below to provide us with the information needed to prepare your Forms 1099-MISC and NEC information returns.

Caution! The Internal Revenue Service matches payee names and taxpayer identification numbers (“TIN”) (e.g. Social Security Numbers (“SSN”) or Employer Identification Numbers (“EIN”) Numbers). It is important that if the payee name is that of an individual that you provide their SSN for the TIN or if the payee name is that of a business that you provide their FEI number for the TIN. Here are several examples of proper name and TIN matching.

Payee TIN matching examples

|

Payee |

TIN | Type | ||

| John A. Doe | 999-99-9999 | SSN | ||

| Sally Smith | 888-88-8888 | SSN | ||

| John A. Doe d/b/a City Handy Work | 999-99-9999 | SSN | ||

| City Handy Work | 99-8888888 | EIN | ||

| Sally Smith Law Firm, LLC | 88-7777777 | EIN | ||

| John and Sally Office Cleaning Partnership | 77-6666666 | EIN |